- Zuber Letter

- Posts

- The Fed broke the housing market—we'll be stuck for years

The Fed broke the housing market—we'll be stuck for years

In this week’s Zuber Letter, I outline some of my U.S. housing market predictions—including my belief that home prices will remain flat for the next few years.

Michael Zuber

June 28, 2024

AI-generated image

Home prices flat until 2030?

Earlier this month, I spoke with Mike Simonsen, the founder and president of real estate analytics firm Altos Research, about what I expect to happen in the housing market in the coming years.

My main prediction: home prices are going to hold flat-ish until almost 2030. Here are some of the key points I made about the future of the housing market in my conversation with Mike:

1. The Fed broke the housing market

The housing market operated in a rather structured mechanism for decades. People would buy an entry-level house and stay there for six to eight years, then, after some career advancement or the family getting bigger, they would sell that home and buy a “move-up” home. They’d be there for another decade or so, then maybe do another “move-up” after that.

That system doesn’t exist anymore. We will see the lowest housing turnover that we've seen since the early 1980s because people either don't want to move—or worse—they won't get approved. With today’s high rates, a lot of folks couldn’t afford to purchase the home they are in today, let alone a “move-up home.”

We are in a “transaction depression,” and probably will be for the next three to five years. While some people say that prices have to come down because rates went from 1 to 5%, I say they don’t.

When you look at history (1987-1990), prices don’t have to fall but transactions will.

2. Builders are going to meet the market, building smaller homes

Since the Great Recession, builders have focused on building big, luxury homes because that's what penciled and only well-off homebuyers were buying. Now that is done. If a homebuilder really wants to make hay they need to build smaller homes.

Last year, the average home size was down 3%, and I think the homes being built will only get smaller in the next year, by 5 to 6%.

Why? First-time homebuyers have no new choices: Current entry-level homeowners aren’t selling. Homebuilders are burning through their entry-level inventory, so they are focused on building more, smaller units.

Some people will say this will lead to “new home prices crashing” but they aren't crashing—builders are just selling smaller homes.

3. The pain is coming for commercial, not residential

I’ve spoken at length about how the pain heading for commercial real estate will be the greatest wealth-building opportunity in our lifetimes. People will make a lot of money cleaning up the mistakes investors made during the pandemic.

We are already seeing this play out. The tallest building in Fort Worth, Texas just sold for 10% of its previous sale.

However, residential is a different story. I think the real median prices for existing single-family home sales will remain flat-ish until 2030. We’ve seen most of the appreciation we are going to see for the decade in its first three years.

I think this is a lot like the 1980s. We might see home prices go up nominally, but if you strip out inflation it will basically be flat.

4. We are in a bifurcated housing market.

Anecdotally, I have heard clean, pretty properties below the median sell fast and above the asking price whereas luxury properties are sitting for longer and seeing price cuts.

So if the data tells us we are seeing 33.7% price cuts, I’d guess the bulk of those price cuts are happening above the median, whereas fewer of those cuts are happening below the median.

When it comes to the trajectory of home prices, It’s important to remember that the top of the market is not going to behave the same way as the bottom of the market.

Number of the week: 5%

I read an article this past week that used data from the Fed's Survey of Consumer Finances to highlight the top 5% net worth threshold by age group. This was the breakdown:

20s: $415,000

30s: $1,104,100

40s: $2,551,500

50s: $5,001,600

60s: $6,684,220

70+: $5,860,400

How do these people get in the top 5%? It’s not rocket science—they own assets. To be in the 95th percentile of your age group, income isn’t enough, you must buy and hold assets for a long time.

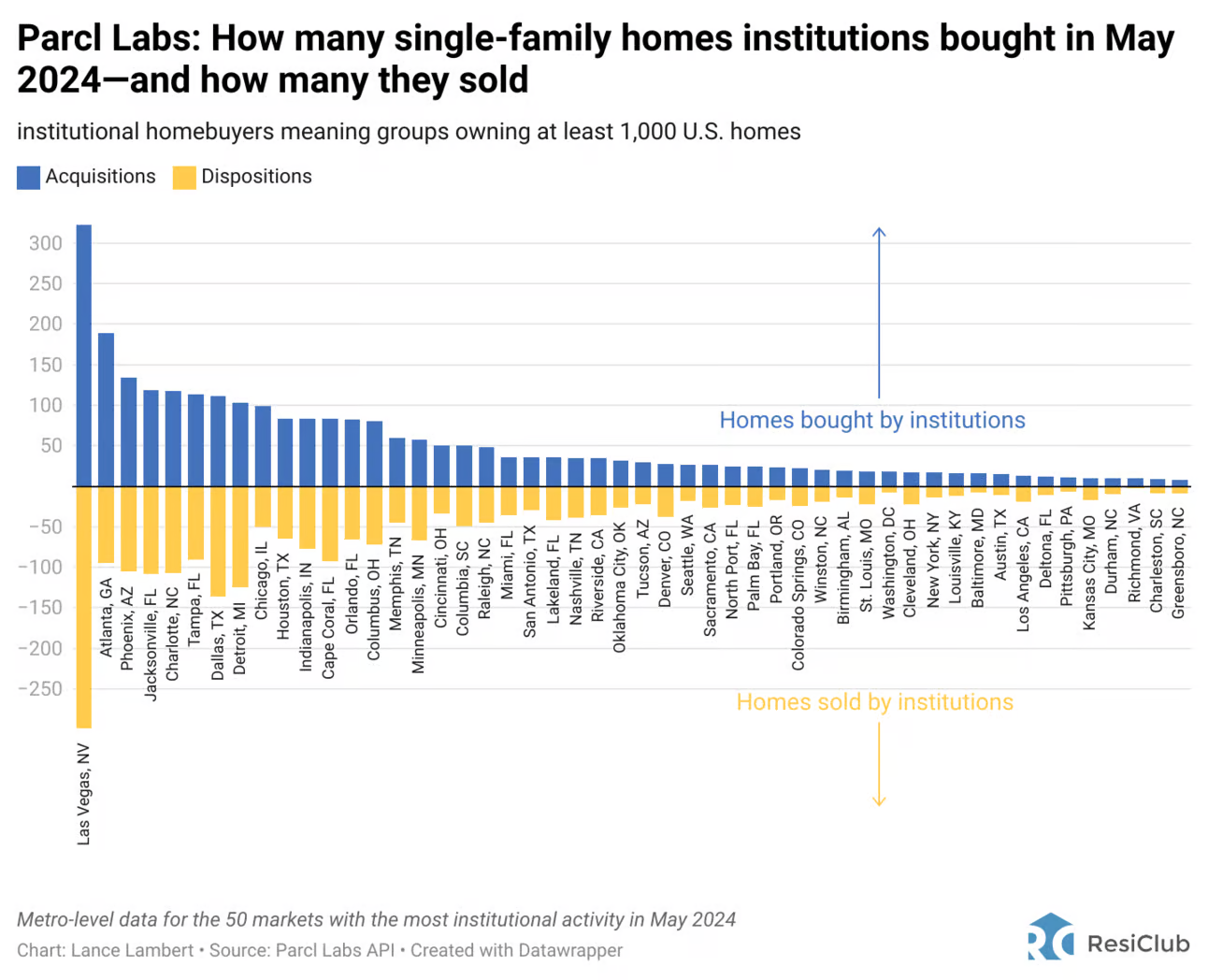

ResiClub Chart of the week:

Last week, ResiClub’s Lance Lambert analyzed Parcl Labs data to see where institutions bought the most homes in May 2024. ResiClub found that despite what some viral social media posts are saying, institutional homebuying is still fairly constrained in 2024.

“While there’s still an appetite to push capital into the build-to-rent sector, institutional scatter-site home buying (i.e. when investors buy up individual homes in the resale market) has been subdued ever since spiked mortgage rates put out the Pandemic Housing Boom’s institutional frenzy,” Lambert wrote.

The chart above shows the number of single-family homes bought and sold by institutions in May 2024.

Join the One Rental at a Time Skool Community

Just a few weeks after our launch, the One Rental at a Time community on Skool is already more than 100 members strong.

We’re creating more opportunities for you to interact with those who have achieved financial freedom through real estate investing.

Being surrounded by people at all stages of their real estate investing journey is crucial to your success, and joining us on Skool is an easy way to do just that.

It is only $20 to gain access to my monthly (or more) live streams as well as various millionaires answering your questions in real-time and connecting with people who can help you.

Learn more about how I am organizing the ORAAT Skool community content and calendar.