- Zuber Letter

- Posts

- Zuber: Still waiting for that housing crash? These 9 reasons explain why it never came

Zuber: Still waiting for that housing crash? These 9 reasons explain why it never came

This week, I was bombarded with messages from housing crash fans. So I decided to do what I always do—stick to the facts.

Michael Zuber

June 23, 2025

Today’s Zuber Letter is brought to you by Stessa!

Track Every Dollar with Stessa—Effortlessly

Managing rental property finances doesn’t have to be a headache. With Stessa, real estate investors can simplify accounting, automate transaction tracking, and stay organized—all in one powerful, easy-to-use platform. Link your bank accounts, property managers, and financial institutions for a clear, accurate financial picture across your entire portfolio.

Stessa also makes bookkeeping stress-free. Track income and expenses by property or portfolio, scan and retrieve receipts on the go, and ensure every transaction is categorized to maximize your deductions. Whether you're managing a portfolio locally or spread out across the country, Stessa keeps you in control from virtually anywhere.

📹 Watch the Demo and see how Stessa can streamline your rental property finances.

✅ Sign Up for Free — Your transactions. Your deductions. Simplified.

Zuber: 9 reasons the housing crash never came

Ever since the Pandemic Housing Boom, a vocal crowd of “doomers” has been warning that a housing crash is imminent. And yet—home prices haven't collapsed. In fact, the crash hasn’t come close to materializing the way they predicted.

Why? Below are nine reasons the housing crash crowd has been consistently wrong, and likely will continue to be. I hope many of you can use this to help tune out the noise and stay focused on what matters.

1. They’re stuck in 2008

Many housing crash predictors have what I call GFC PTSD—they assume every cycle must end like the global financial crisis. But if you zoom out and study the last 50+ years, you’ll see that 2008 was an extreme outlier, not the norm.

2. They ignore history

It’s harsh but true: some of these crash callers are either too young, too naïve, or too lazy to study real estate history. If they had, they’d know the U.S. has seen rapid rate hikes before—and home prices didn’t collapse then either. Smart investors learn from past cycles. The crash crowd clearly hasn’t.

3. We already had a crash—in transactions

From 6.4 million home sales down to 4 million (and falling). That’s a 35%+ drop. That is a crash—it just didn’t happen in prices. It showed up in volume, commissions, jobs, and GDP. And most doomers completely missed it.

4. They don’t understand price elasticity

Single-family homes are inelastic. They don’t trade like stocks or crypto. Sellers don’t slash prices overnight, and inventory doesn’t flood the market all at once. This is a slow-moving asset class, and history confirms it.

5. They forget shelter is essential

People don’t walk away from 2.8% mortgage rates easily. In 2008, many borrowers had exploding ARM loans and could rent for far less than their mortgage payment. Today, it’s the opposite—owners are locked into cheap housing, and rent is usually more expensive. That dynamic changes everything.

6. They don’t grasp foreclosure timelines

In the GFC, it often took 1,000 days from last payment to foreclosure. That’s nearly three years. Today’s distressed FHA borrowers may eventually lose their homes—but you won’t see that inventory until 2026 at the earliest. A foreclosure wave in 2025? Not happening.

7. They underestimate the government’s response

After the GFC, policymakers learned their lesson. Forbearance, rescue programs, and regulatory backstops will prevent another freefall. The Fed and Treasury will not let housing spiral the same way twice.

8. They bet on a rare event

A drop of 10% or more in a single year? That’s extremely rare. Outside of the GFC, U.S. housing prices rarely fall more than 5% in a given year. Declines can happen—but big, fast crashes are statistical outliers, not base cases.

9. They’ve sold out to the algorithm

The real motivation behind doom content? Clicks. Fear drives engagement. That’s why so many of these creators post “crash” videos daily—because it pays. And ironically, some of the loudest crash callers are now buying homes themselves.

They profit from your paralysis. Many are failed insiders: including mortgage originators, real estate agents, and underwriters. Some of the loudest crash voices failed in the industry and found a new hustle: monetizing fear. Don’t let them rent space in your head.

Ask yourself: Are you reacting to facts—or fear? Are you learning from history—or headlines? This market is hard, but it’s not 2008. And the more you do the work, the more clearly you’ll see that.

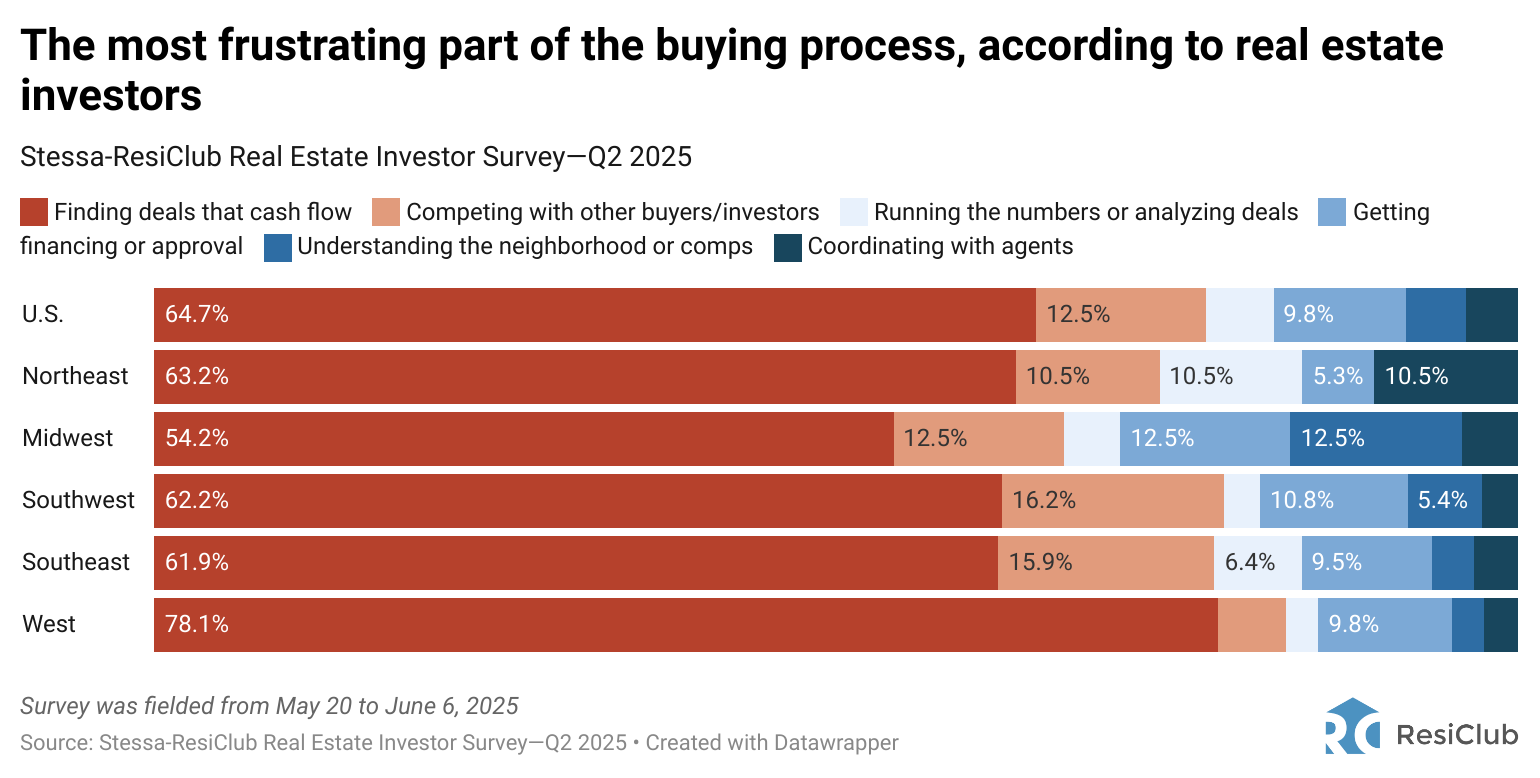

ResiClub chart of the week:

This past week, ResiClub’s Meghan Malas released results from a recent survey ResiClub conducted with Stessa, an asset management and accounting software for real estate investors, owned by Roofstock.

Among the findings, Meghan reported that 65% of surveyed real estate investors said the most frustrating part of the buying process right now is finding deals that cash flow. Among respondents based in the West, that number was 78.1%.

Despite the struggle to find deals that pencil, the survey also found that 45% of U.S. real estate investors say they plan to grow their portfolios in the near term.

Here are some other key findings from the survey:

Half of surveyed real estate investors (50%) said they’d accept a mortgage rate up to 7.00% on their next purchase.

58% of real estate investors say they self-manage their properties.

20% say they first look at off-market deal sources.

When it comes to the search, real estate investors say Zillow is the most helpful platform, with more than 70% considering it “very helpful” or “somewhat helpful.”

Want to advertise your business on The Zuber Letter? Email [email protected]